During the second quarter of 2016, real estate firm Colliers International reported that apartment sales performance in Jakarta continued to languish, with a moderate 0.5 percent growth in price compared with the previous quarter.

There were 4,777 new units from the handover of a total of eight apartment towers from five projects. The cumulative supply of strata-title apartments in Jakarta grew by 2.9 percent quarter-on-quarter (QoQ) or 12.4 percent year-on-year (YoY) to a record 167,697 units.

Prices of apartments have been relatively flat as most of the projects held prices in order to attract buyers. The average asking price of apartments in Jakarta was recorded at IDR 31 million per sqm, increased modestly by 0.5 percent QoQ.

In terms of supply, Jakarta will see an additional 15,442 units during the remainder of 2016 and a total 25,222 units in 2017. Although the market saw an increase in launching activity, buying sentiment has remained lukewarm; investors and end-users are holding their plans to buy apartments in view of the current economic slowdown. Colliers noted that take-up rates will continue to hover at between 86 percent and 87 percent.

Given a drop in the expatriate community, Colliers said that it expects asking rental rates will remain unchanged until the end of 2016. It also predicts a 9 percent to 11 percent increase in the average asking price for apartments for sale due to the higher prices quoted by future apartment projects which will open by the end of the year.

Supply

By the end of the second quarter of 2016, cumulative supply of strata-title apartments in Jakarta had grown at a moderate pace of 2.9 percent QoQ, equal to 12.4 percent YoY, to a record 167,697 units. During this quarter, the market received 4,777 new units from the handover of eight apartment towers in five projects, including The Green Pramuka, Royal Springhill, Bassura City, Casablanca East Residence and 19 Avenue. In terms of market segment, middle-lower class apartments dominate the current additional supply at 86.4 percent of three projects located in non-prime areas.

Green Pramuka City (Orchid and Penelope Towers) and Royal Springhill (Bouvardia and Bulgari Towers) are both located in Central Jakarta; however they are targeting different market segments, i.e. middle-low and middle-upper, respectively. Meanwhile, East Jakarta continued to see new middle-low class projects from the opening of Bassura City (Edelweiss Tower) and Casablanca East Residence (Dallas & Casablanca Towers). In West Jakarta, 338 additional units came from the completion of a mid-rise apartment project, 19 Avenue (Tower A). 19 Avenue was previously a stalled Rusunami (low-cost apartment) project called Orchard Place Residence, developed by PT Bintang Milenium Indonesia. It was acquired by Margahayu Land, who changed the name.

Targeting the same low segment, fully furnished 19 Avenue (Tower A) apartments are offered at prices ranging from IDR 400 million to IDR 600 million per unit.

As of the middle of 2016, about 40.6 percent of the 26,583 projected units which will be completed this year have been handed over, leaving about 15,793 units to be handed over in the next semester.

Newly Launched Projects

During this quarter, Jakarta’s apartment market saw a moderate addition of newly launched/introduced projects. Four new projects with 5,946 units initiated pre-sale activities in Q2 2016 and are expected to be completed in the next four years. The number of units being introduced/launched is 20 percent lower than the same period in 2015. This suggests that developers are generally quite cautious over the current market condition, with considerable supply going forward and, to some extent, slow absorption, noted Colliers.

East Jakarta hosts about 87 percent of the total newly introduced/launched units from two projects: East 8 and Prajawangsa City. East 8, developed by Karya Cipta Group, is targeted at the middle-lower segment, particularly workers in the surrounding areas. East 8 apartment is located in a settled residential area and will benefit from easy accessibility to public transportation, including the future LRT and the existing Jagorawi toll road.

With a similar target market, Prajawangsa City, developed by Synthesis Development, together with St. Carolus Vereeniging, claims to be an improvement on their previous project, Bassura City, with bigger units and more green space.

Another new project by Synthesis Development is Samara Suites, which was previously launched as The Residence at Gatot Subroto, which offered bigger units and higher prices. Subsequently, the developer revised the concept, including the floor plan, unit size and pricing strategy, in order to meet the budget of buyers. As of the end of May, 60 units in Samara Suites have been booked. Another project located in a so-called expatriate area,

Lavish Kemang Residence is developed by PT Kemang Karya Utama, which has extensive experience in developing houses and townhouses for expatriates.

The total number of apartment units launched during 2Q 2016 was 5,946. The mood in the apartment market has been subdued, as reflected in the limited number of newly introduced/launched projects in recent quarters. In general, some developers have opted to postpone the launch date of their projects due to a lack of confidence in the current market situation. Moreover, the overall Indonesian economy faces a number of downside risks, such as slow economic growth and lowered consumer confidence, which impacts project decisions by developers.

Demand

No significant changes in the apartment market were noted in 2Q 2016 by Colliers. Although the market saw some improvement in launching activity, buying sentiment remained lukewarm. Sales remained quiet as investors and end-users have put their plans to buy apartments on hold in view of economic conditions. Prospective buyers continued to tread with caution and be mindful with their purchases in light of recent market conditions, particularly delays in construction progress and project cancellations, which were further worsened by the lack of regulations protecting buyer and developer rights.

Overall, the average take-up rate only rose by less than 1 percent QoQ and YoY.

A combination of creative marketing strategies (with gimmicks, etc.) and a limited number of newly introduced/newly launched projects have helped lift, or at least maintain, the overall take-up rate performance of the apartment market in Jakarta.

The unrevealed fact behind the vigorous sales performance in certain projects, noted Colliers in its report, is insider trading with buyers who could be shareholders or top executives of the company. Though small in number, such transactions helped lift overall sales performance. Another way to boost sales is to offer buy-back and cash-back guarantees, i.e. refunding the money to the buyer when the handover schedule does not meet the agreed timeline.

Developers have collaborated with insurance companies to provide protection for their apartment units with the benefit of 100 percent cash-back after 15 claim-free years. As long as buyers don’t make a claim on their apartment insurance (also called Building Insurance) policy for 15 years, they will receive a full refund of all of the Building Insurance premiums that they have paid.

In terms of area, under-construction projects in the CBD recorded the highest increase in overall take-up rate, at 2.5 percent, compared with 1.1 percent and 1 percent in South Jakarta and non-prime areas, respectively.

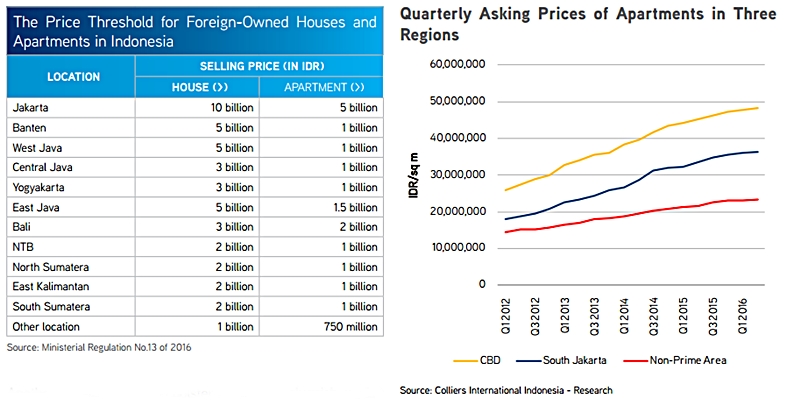

Thus far, foreign ownership regulations have not changed drastically because they still have to comply with the Agrarian Law, which limits the scope of ownership. Foreigners can only buy property under a Hak Pakai (Right to Use) title, and in order to do that they have to hold a legal stay permit in Indonesia.

Recently, after the issuance of revised Government Regulation number 103/2015, the Government (Head of the National Land Agency) introduced the implementation of the regulation No. 13 of 2016 on Procedures for Granting, Relinquishing and Transferring Ownership of Residential Property for Foreign Citizens Domiciled in Indonesia. This new regulation makes it clearer that foreign citizens are only allowed to own high-end residential properties (either apartment or landed house) with various minimum thresholds based on the property type and location.

Previously, Indonesian authorities had announced last year that foreigners would be allowed to purchase apartments or houses which cost at least IDR 10 billion per unit (roughly US$ 740,000) under a right-to-use title. Nonetheless, even with these government efforts to ease regulations on foreign ownership, the main challenge facing apartment sales remains: they have to be built on Right to Use land that is unconventional in the local market.

Another appealing effort to bolster the current sluggish market has come through relaxation of LTV regulations. The Central Bank (Bank Indonesia) has stepped in to support the domestic economy and property market and, in particular, is likely to boost apartment sales going forward. Bank Indonesia is planning to review loan-to-value (LTV) regulations to boost the property market in 3Q 2016. Under the easing policy, the Central Bank will reduce the amount of down payments in a bid to spur credit growth and boost economic growth. Another possible measure would let homeowners take out loans to purchase a second home “off the plan”, or one that is under pre-construction. This relaxation would provide a tailwind to the property sector, particularly the apartment market, if it is fully materialised.

Nevertheless, Bank Indonesia has repeatedly emphasised that it will continue to closely monitor the market and enforce policies to prevent the property market from overheating, which could lead to a bubble. It will also maintain a prudent policy to keep non-performing loans below 5 percent of total loans.

Asking Prices

Overall, the prices of apartments in Jakarta have been relatively flat, as most projects have maintained prices in order to attract buyers in this softening market situation. Newly launched or introduced projects are offered at a lower price compared to the average market prices, which may hamper further price growth.

To a greater extent, developers are quite concerned over the weakened purchasing power of general consumers, which is reflected in the latest data from the Statistics Bureau Indonesia, where GDP only grew 4.92 percent during the first quarter of 2016, slower than the estimate of slightly above 5 percent. Therefore, in order to cope with such a situation, developers have mainly played the role of a bank by providing installment schemes as their default payment method. Moreover, in some cases, developers have offered additional discounts, ranging from 3 percent to 5 percent, depending on the installment period, meaning that longer installments receive a smaller discount.

As of Q2 2016, the average asking price of apartments in Jakarta was recorded at IDR 31 million per sqm, a modest increase of 0.5 percent QoQ and 9 percent YoY. In South Jakarta apartment prices rose by 1.1 percent QoQ and 11.3 percent YoY, the highest rate compared with the CBD and other non-prime areas.

South Jakarta remains a desirable location to live in, as indicated by the sales improvement during the reviewed quarter. In addition, some developers raised selling prices because their projects are approaching handover. The CBD still has the highest apartment prices, at IDR 48.3 million per sqm, an increase of 0.9 percent compared to the previous quarter, while non-prime areas posted the lowest QoQ growth, 0.7 percent, to IDR 23.3 million per sqm, mainly because the newly introduced projects in East Jakarta are offered at a lower price than the market average.